Welcome on Stéphane Crépey’s web page

|

I am professor at the Mathematics Department of Evry University, where I am in charge of the MSC Financial Engineering. My research

interests are financial modeling, counterparty and credit risk, numerical

finance, and related mathematical topics in the fields of backward

stochastic differential equations and partial differential equations o Email stephane.crepey@univ-evry.fr o Address Université d'Evry, Laboratoire Analyse

& Probabilités, Bâtiment IBGBI, 23 Boulevard de France, 91037 Evry cedex

(RER D Evry Courouronnes). Office 324 (3ème

étage). Tel +33 (0) 1 6485 3480 (secr. 3488) |

Get some of my works

·

Working

Papers

- S.

Crépey and S. Song. Counterparty risk

and funding: Immersion and beyond. Revised.

- S. Crépey,

A. Macrina, N. Nguyen and D. Skovmand. Rational multi-curve models

with counterparty-risk valuation adjustments. Submitted.

- S.

Crépey and S. Song. Invariant times. Submitted.

·

Financial Modeling

- Multiple Curves

- S. Crépey,

Z. Grbac, N. Ngor and D. Skovmand. A Lévy HJM

multiple-curve model with application to CVA computation.

Forthcoming in Quantitative Finance.

- S. Crépey and R. Douady. LOIS: Credit and Liquidity. Risk

Magazine June 2013. Short version The Whys of the of the LOIS: Credit Skew and

Funding Rates Volatility Bloomberg Brief / Risk 24 May 2013, p.6-7

- S. Crépey, Z. Grbac and H. N. Nguyen. A

multiple-curve HJM model of interbank risk. Mathematics and

Financial Economics 6(3) 155-190, 2012.

- Funding

- S. Crépey. Preface

to the special issue ‘Frontiers of Counterparty Risk’, International

Journal of Theoretical and Applied Finance March

2013.

- S. Crépey,

R. Gerboud, Z. Grbac

and N. Ngor. Counterparty Risk and Funding: The Four

Wings of the TVA. International Journal of Theoretical

and Applied Finance March 2013.

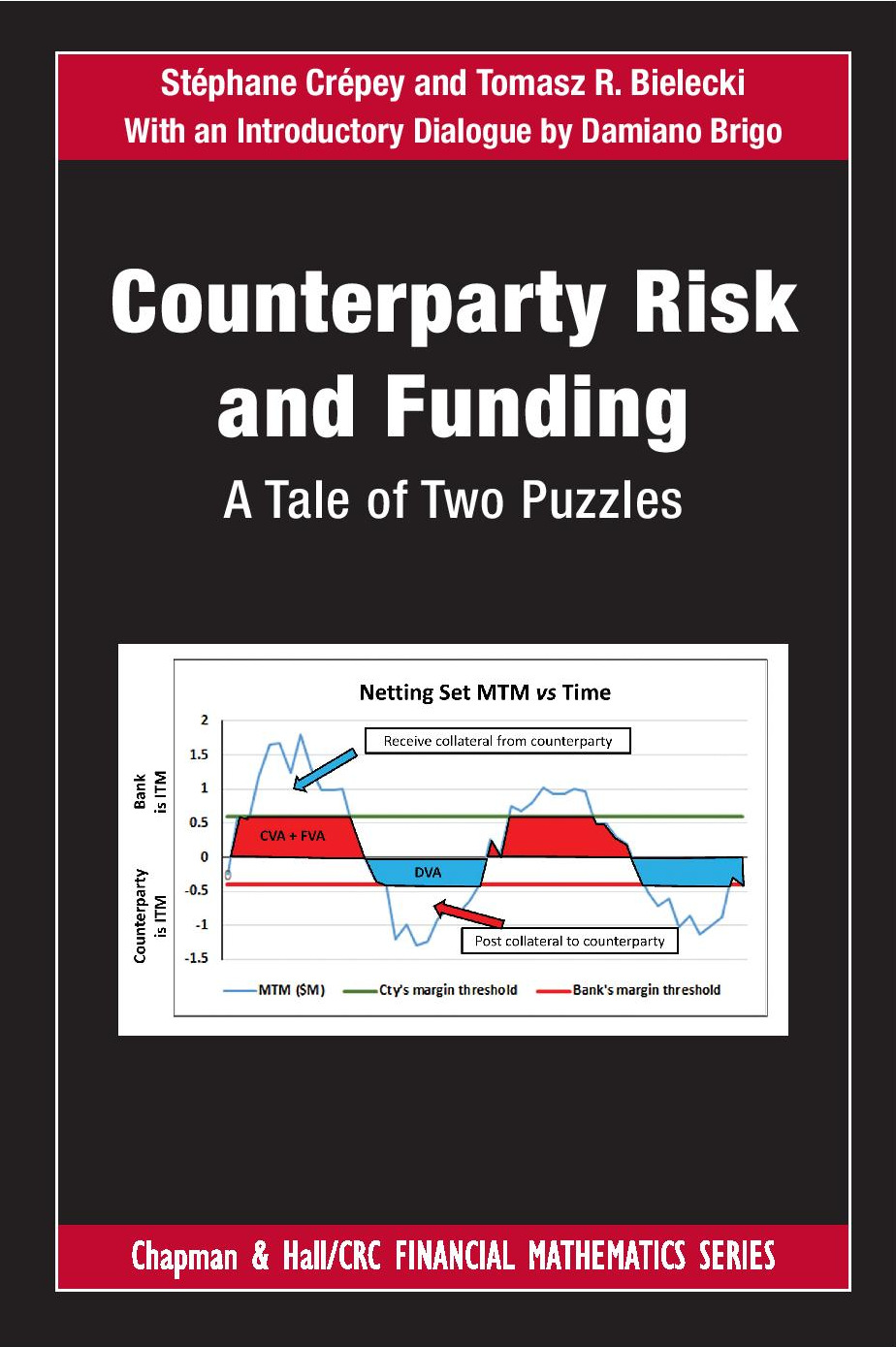

- S. Crépey. Bilateral

Counterparty Risk under Funding Constraints – Part I:

Pricing and Part II: CVA. Mathematical Finance online first January

2013. See

also: S. Crépey. Counterparty

risk and funding: putting things together. Creditflux

Newsletter Analysis, p.14-15, Dec 2011.

- Counterparty Credit Risk

- S. Crépey,

M. Jeanblanc and D. L. Wu. Informationally Dynamized Gaussian Copula. International

Journal of Theoretical and Applied Finance March 2013.

- T. Bielecki, S. Crépey. Dynamic Hedging

of Counterparty Exposure. Forthcoming in The Musiela

Festschrift, T. Zariphopoulou, M. Rutkowski and Y. Kabanov, eds, Springer Berlin.

- S.

Assefa, T. Bielecki,

S. Crépey, M. Jeanblanc. CVA computation for counterparty risk assessment

in credit portfolios. Short version of the paper forthcoming under

the same title in the book Credit Risk Frontiers, T. Bielecki, D. Brigo and F. Patras, eds, Wiley (Hard-copy of the long, copyrighted

version, available upon e-mail request).

- T. Bielecki, S. Crépey, M. Jeanblanc

and B. Zargari. Valuation and

Hedging of CDS Counterparty Exposure in a Markov Copula Model. International Journal of Theoretical and Applied Finance 15 (1) 1250004, 2012.

- S.

Crépey, M. Jeanblanc and B. Zargari. Counterparty Risk on a CDS in a Markov

Chain Copula Model with Joint Defaults. Recent Advances in Financial

Engineering

o

Portfolio Credit Risk

- T. Bielecki, A. Cousin, S. Crépey, A. Herbertsson.In

search of a grand unifying theory. Creditflux

Newsletter Analysis, p.20-21, July 2013. Web full version The

Bottom-Up Top-Down Puzzle Solved, creditflux.com

- T. Bielecki, A. Cousin, S. Crépey, A. Herbertsson. Dynamic

Hedging of Portfolio Credit Risk in a Markov Copula Model. Forthcoming

in Journal

of Optimization Theory and Application.

- T. Bielecki, A. Cousin, S. Crépey, A. Herbertsson. A Bottom-Up Dynamic Model of Portfolio Credit Risk - Part I: Markov Copula Perspective and Part II: Common-Shock Interpretation, Calibration and Hedging issues. Recent Advances in Financial Engineering 2012, World Scientific, forthcoming.

- A. Cousin, S.

Crépey and Y.-H Kan. Delta-hedging Correlation Risk? Review

of Derivatives Research 15 (1) 25-56, 2012.

- T. Bielecki, S. Crépey, A. Herbertsson. Markov Chain

Models of Portfolio Credit Risk. Short version of the paper

forthcoming under the same title in Oxford Handbook of Credit Derivatives,

A. Lipton and A. Rennie, eds (Hard-copy of the long, copyrighted version, available upon

e-mail request).

§ T.R. Bielecki,

S. Crépey, M. Jeanblanc. Up and Down Credit Risk. Quantitative

Finance 10 (10)

1137-1151, 2010.

§ T.R. Bielecki, S. Crépey, M. Jeanblanc and M. Rutkowski. Valuation of Basket Credit Derivatives in the Credit Migrations Environment. Handbook of Financial Engineering, 2007.

- Defaultable Game Options

- T.R. Bielecki,

S. Crépey, M. Jeanblanc and M. Rutkowski. Convertible Bonds in a Defaultable Diffusion Model. Convertible Bonds in a Defaultable

Diffusion Model. Stochastic Analysis with Financial

Applications, A. Kohatsu-Higa, N. Privault

and S.J. Sheu eds,

p. 255-298, Birkhäuser / Springer Basel,

2011.

- T.R.

Bielecki, S. Crépey, M. Jeanblanc

and M. Rutkowski. Defaultable Options in a Markovian Intensity Model of Credit Risk. New Updated

Version of the paper published under the same title in Mathematical Finance, 2008.

- T.R.

Bielecki, S. Crépey, M. Jeanblanc

and M. Rutkowski. Valuation and Hedging of Defaultable Game Options in a Hazard Process Model. Journal of Applied Mathematics and

Stochastic Analysis,

Article ID 695798, 33 pages, 2009 (and Long Preprint Version).

- T.R.

Bielecki, S. Crépey, M. Jeanblanc

and M. Rutkowski. Arbitrage Pricing of Defaultable Game Options with Applications to

Convertible Bonds. Quantitative

Finance, Volume 8,

Issue 8 December 2008 , pages 795 - 810.

- Local Volatility

§ S. Crépey. Delta-hedging

Vega Risk? Quantitative Finance 4, p.559–579, 2004.

·

BSDEs and/or

PDEs

- S.

Crépey and S. Song. BSDEs of counterparty risk. Forthcoming in Stochastic

Processes and Applications.

- J.-F. Chassagneux

and S. Crépey. Doubly reflected BSDEs with Call

Protection and their Approximation. ESAIM: Probability

and Statistics, forthcoming.

- S.

Crépey. About

the Pricing Equations in Finance. Paris-Princeton Lectures in

Mathematical Finance 2010, Lecture Notes in Mathematics, Springer, p.63-203, 2011.

- S.

Crépey, A. Matoussi. Reflected and Doubly

Reflected BSDEs with Jumps: A Priori Estimates and Comparison Principle. Annals of Applied Probability, Vol

18, Issue 5 (October 2008), p. 2041-69.

- S.

Crépey Calibration of the local volatility in a generalized

Black-Scholes model using Tikhonov

regularization. SIAM

Journal on Mathematical Analysis, Vol

34 No 5 (2003), p. 1183-1206.

·

Numerical

Finance

- Calibration

- T. Bielecki, A. Cousin, S. Crépey, A. Herbertsson.

A

Bottom-Up Dynamic Model of Portfolio Credit Risk with Stochastic

Intensities and Random Recoveries. Communications in Statistics – Theory and Methods, forthcoming.

- S.

Crépey. Tikhonov Regularization. Encyclopedia

of Quantitative Finance,

editor Rama Cont, p. 1807-1812, 2010.

§ S. Crépey. Calibration

of the local volatility in a trinomial tree using Tikhonov

regularization. Inverse Problems, 19 (2003), p.

91-127.

- Monte Carlo

- S.

Crépey and A. Rahal. Simulation/Regression Pricing

Schemes for CVA Computations on CDO Tranches. Communications in

Statistics – Theory and Methods, forthcoming.

- S.

Crépey and A. Rahal. Pricing Convertible Bonds with Call Protection. Journal

of Computational Finance Vol.15 Num. 2, 37-75, Winter 2011/12.

- R.

Carmona, S. Crépey. Particle Methods for the Estimation of Markovian Credit Portfolios Loss Distribution. International Journal of Theoretical and Applied Finance Vol

13, Issue 4, p. 577-602, 2010.